Call us: 01865 842 266

Email us: [email protected]

Oxford Accountants Helping Local Businesses Thrive

Brookwood is a long established Oxfordshire accountancy firm that puts clients first. Whether you are a business or an individual our personalised approach ensures that our expert team will work with you to provide a service tailored to your needs and guidance you can trust.

Personalised accountancy services for businesses, landlords and individual taxpayers.

Businesses:

For nearly 40 years Brookwood has expertly supported businesses. For SMEs who need strategic financial guidance, our firm provides advisory and personalised tax services. Unlike larger accountancy firms that treat growing businesses as numbers on a spreadsheet, we invest heavily in understanding our clients’ unique goals so that we build long term success together. Whether you are a new start-up or an established and growing expert business in your industry, your firm will benefit from our guidance.

Whatever success looks like to you, we have the advisory, tax and accountancy services you need to make a positive impact on your business. In a changing business landscape, we continue to advise and guide SMEs in navigating the challenges of doing great business.

Individuals:

At Brookwood we safeguard busy professionals, landlords and individual taxpayers from the stress of changing HMRC requirements. By managing your entire personal tax affairs, we ensure complete compliance, protect you from rising HMRC penalty points and interest charges, and replace tax anxiety with peace of mind.

We help our clients achieve a secure future for themselves and their families through inheritance planning. Our experienced personal tax team provides expert advice for individuals resident in the UK and internationally.

Our Accountancy Services

We have tailored all our accountancy offerings to give you the correct level of support immediately, with the flexibility to adapt as your business grows.

Bookkeeping

Daily bookkeeping to ensure your records are accurate, organised, and VAT-ready.

Tax & Compliance

Tax returns, filings, and compliance checks handled accurately and submitted on time.

Payroll

Reliable payroll processing to keep your team paid correctly and on schedule.

Specialist Tax

Personal tax returns, Self Assessment, and rental income handled with expert care.

Financial Forecasting

Forward-looking financial models to help you plan, budget, and make confident decisions.

Company Secretarial

Statutory filings, company records, and Companies House obligations taken care of.

Virtual Finance Director

Senior financial oversight and strategic insight, without the cost of a full-time hire.

HMRC Enquiries

Daily bookkeeping to ensure your records are accurate, organised, and VAT-ready.

TESTIMONIALS

What Our Oxfordshire Clients Say

Our clients stay with us because they value our continuity, reliability, and the peace of mind that comes from having an expert on their side at key times.

"The Brookwood team have been our accountants for our three companies since 2006. We are delighted with their services and feel valued as a loyal customer."

- M Davis

"As a client for more than 20 years, I have always found Brookwood highly efficient, quick to respond and very helpful, offering advice and excellent support whenever its been required."

- M Potts

"Everyone is extremely helpful from small details to important tasks. Thank you for excellent service over 10 years."

- A Waterhouse

What Level of Support Do You Need?

No two businesses look the same, and the level of support you need will change over time. At Brookwood, we tailor our services around where you are now and where you want to get to.

1. Just the Essentials

This option suits business owners who want the basics handled properly. We take care of accounts, tax and statutory submissions so you stay compliant, without unnecessary complexity or add-ons.

2. Accounts with Support and Guidance

Designed for businesses planning ahead. Alongside compliance, we provide regular reviews, business valuations, and competitor insights to support growth, succession, or future sale planning.

3. Fully Managed, Next Level

Leave the day-to-day bookkeeping and accounts to us. We manage your finance function, systems and reporting, supported by advisory input and access to coaching and mentoring when needed.

4. Cloud Wealth Club

For cloud accounting clients who want ongoing support and accountability. Access practical tools, regular updates, and peer support via structured sessions focused on performance.

5. Business Development, Business Coaching & Mentoring

Focused on accountability and direction. This level supports business owners who want structured guidance, regular check-ins and mentoring to help avoid common pitfalls and stay aligned with their goals.

6. Virtual Finance Director

Senior-level financial support tailored to your business, without the commitment of a full-time FD. From day-to-day decision support to board meetings, growth planning or acquisitions, you gain experienced financial leadership as you need it.

Why Oxford Businesses Choose Brookwood

Brookwood has more than four decades of backing businesses within Oxford.

Local knowledge supporting Oxfordshire businesses for over 40 years.

Personal, approachable experts committed to long-term relationships.

Consistently clear advice that allows you to make decisions with confidence.

Comprehensive support covering compliance, growth planning, and mentoring.

Proactive tax planning designed to enhance your overall profitability.

Contact us today to find out how we can support your business.

Meet the Brookwood Team

We are an Oxfordshire-based team of Accountants, Bookkeepers and Virtual Finance Directors. We pride ourselves on our approachable nature and our passion for working with local business owners. We strive to keep our services transparent, professional, and relevant.

Roger Farrell

CIMA Adv Dip MA, AAS, BSc

Director

Sophie Burborough ACCA

Accountant

Katy Ward ACCA

Accountant

Amy Johnson

Digital Comms and Branding

Rita Behal

Practice Manager & Accounts Assistant

Tracey Seymour

Bookkeeper & Cloud Accounting Support

Kay Honour

Bookkeeper & Payroll Administrator

Alanna Thomas BSc

Trainee Accountant

Megan Sero-Jones

Social Media and Marketing Assistant

Alena Čieškovā

VFD Support Manager

Adam Norman

Trainee Administration Assistant

Kiran Dhokia

Junior Accountant

Gus

Company Mascot

Need help filing a self-assessment tax return in Oxford?

We are a straight-talking team and would be happy to discuss your requirements. We prefer real conversations over hiding behind emails, and we are proudly based in your local community.

Pop in to see us at 19 Banbury Road, The Old Post Office, Kidlington, Oxford OX5 1AQ or give us a call on 01865 842 266.

Get in Touch

If you get in touch today, we can get started book a Free Half Hour consult

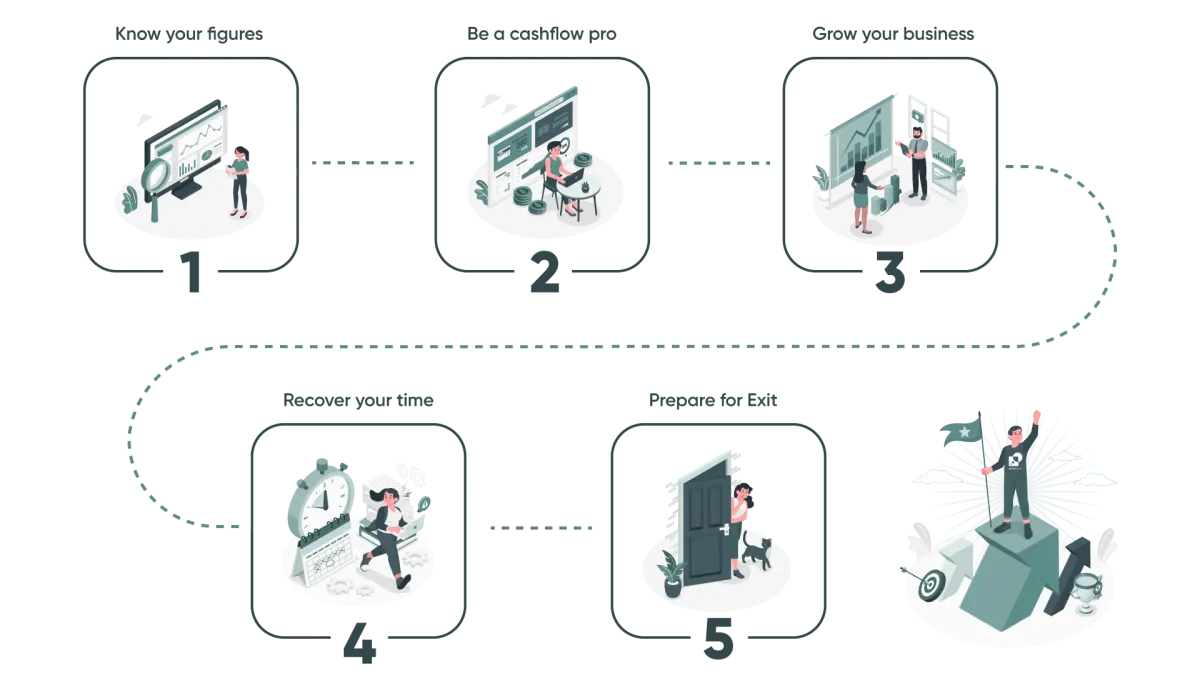

How Brookwood Works

Business News & Oxford Insights

Clear news, updates, and practical tips on tax, HMRC compliance, and managing your business efficiently.

Loading latest insights...

Knowledge Hub

Sign up to keep up to date

© 2024 Brookwood Accountancy Limited is a company registered in England and Wales Registration Number: 03734519

Registered Office: The Old Post Office, 19 Banbury Road, Kidlington, Oxford OX51AQ

Call us: 01865 842 266